It has been another period of declines for almost all asset classes. The problems of inflation, energy, cost of living, central bank interest moves and regrettably war in Ukraine continue to weigh heavily on markets. The new leaders of the UK Government compounded the distress by initiating a budget that has severely damaged the economy. Their reckless actions have resulted in the pound crashing, mortgage rates increasing, gilts crashing, some pension funds put under huge stress and the longer-term outcome will be higher inflation and damage to the property market. It was a very expensive mistake and such an unnecessary folly to ignore the many accurate warnings. It was compounded by dismissing the well-established processes to provide checks and balances. It was catastrophic and the very dire financial explosion only avoided by the rapid intervention of the Bank of England.

Whilst the culpable chancellor and prime minister have now departed, the consequences remain, and it will be the new leadership will need to repair the damage to the UK’s economy and reputation. The early signs are encouraging.

Some of the glimmers of light that we saw earlier in the summer have been extinguished as inflation continues to be elevated and interest rates move upwards much faster that could ever have been imagined a year or two ago. The war continues with no end in sight. The impact on assets has been severe.

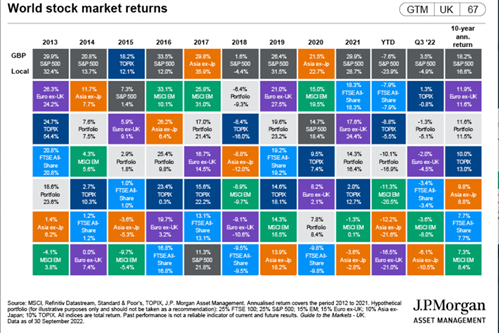

The charts produced by J.P. Morgan show returns over many time periods computed in sterling and local currency.

The year-to-date figures make grim reading as world markets struggle with multiple economic and geopolitical events that are creating huge uncertainty and volatility. One fund manager said recently things are not bad but uncertain. Also, movements can be a little exaggerated as trading volumes are low.

What has been experienced in fixed income or lower risk assets has been extraordinary. Records are sparse, but it is believed to be the worst ever period. Fixed income assets should provide a foundation to portfolios and should provide a negative correlation to higher risk assets, notably equities. This has not happened. Both equities and fixed income have declined hand in hand.

Fixed income in a low interest and indeed sometimes negative interest world has been challenging. That environment has changed. However, this should provide scope for managers to recover. One of the corporate bond funds we support is calculating a yield on the fund of 7%. Lower than current inflation but higher than expected inflation over the years ahead. Higher than dividends. This a huge turnaround in sentiment and opportunity. This is not isolated to one fund.

Everyone wants to know when these horrid market conditions will be behind us. That is almost impossible to know and there is no consensus other than once it is believed peak interest rates and inflation have been reached then markets might begin to pivot towards recovery. Some early signs that interest rates might not be rising as high as recently priced in. The peak and pivot point could be early next year, but realistically it might take longer. No one can forecast that accurately. The manager of one of the world’s top-performing hedge funds through the market turmoil of 2020, recently said that the unwinding of central banks’ vast stimulus programmes to combat high inflation could lead to “doldrum” markets for a prolonged period. He stated quantitative tightening is going to be a real headwind for investors. Few would argue against that sentiment. Whether he’s right we will see.

However, it is worth remembering the famous quote “It’s never as good as it looks and it’s never as bad as it seems.” The chart again from J.P. Morgan shows the duration of Bull (up) markets and Bear (down) markets in the S&P500. The post financial crisis saw a lengthy bull market which produced strong returns.

Despite how it feels, bear markets do end and as we can see can often be quite short. Historically, bear markets are shorter than bull markets. We are already 9 months into the bear market so maybe we are further down the road than it feels and ready to emerge. We are nearer the end today than we were yesterday or last month or 6 months ago. Hopefully, it is darkest just before dawn, or at worst, dawn is not far away. We are beginning to receive more positive sentiments from fund managers which is encouraging. Certainly, there will be greater value in markets but what we are all keen to know is when the positive sentiment translates into recovery. Fixed income might, just might, be the starting point.

The above article is intended to be a topical commentary and should not be construed as financial advice. Past performance is not an indicator of future returns. Any news and/or views expressed within this document are intended as general information only and should not be viewed as a form of personal recommendation.

%MCEPASTEBIN%