A Bumpy Start

2026 has got off to a tumultuous start. Yet again, the USA and in particular Donald Trump, has dominated the news. We have witnessed the rather unpleasant attempted bullying of Greenland that caused significant concern amongst western allies. Ukraine continues to be under attack, and an equitable peace settlement seems to be continually elusive despite the efforts and guidance of the USA which at times are very hard to comprehend. Meanwhile, the tone of Marco Rubio’s February speech at the Munich Security Conference came as a surprise but probably nothing’s changed. Back in the USA we saw some disturbing TV footage of immigration and customs enforcement agents in lethal action. At home in the UK, the political landscape is hugely unsettled and unemployment is rising. As February ended and March begins we witnessed a USA led military strike on Iran that took out the head of state, but has resulted in much retaliation across the region. It would seem inevitable that a period of volatility and market uncertainty will follow until the impact across the region becomes clearer. Donald Trump indicated that it would be a 3- or 4- day action but has now revised that to 4 to 5 weeks.

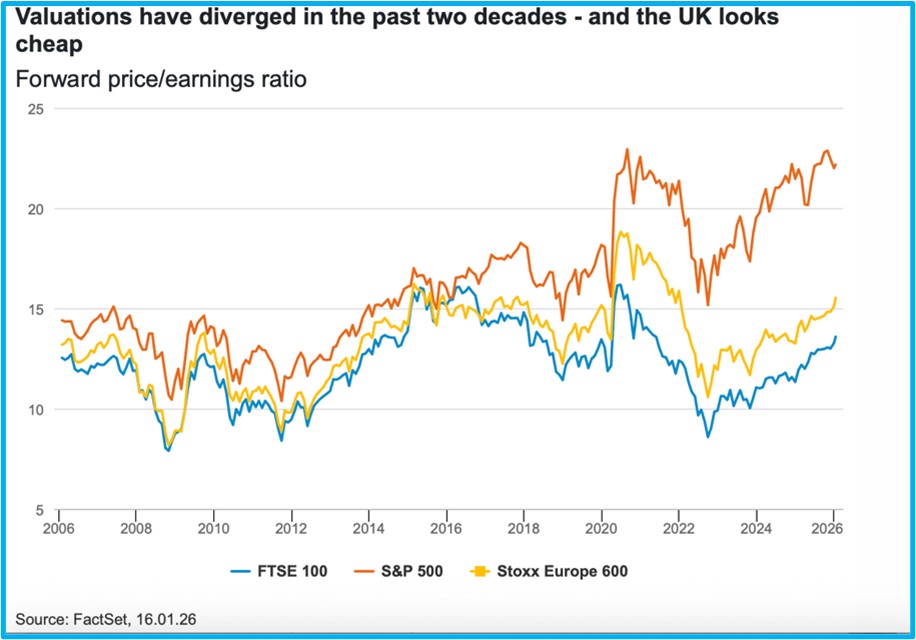

FTSE 100: Strength Amid Uncertainty

A very troubled global picture continues to confront us; However, the UK is on a roll. The UK FTSE 100 index rose by more than a fifth in 2025, beating both the US and Europe in local currency terms. It has gone on to hit new highs in January, and analysts think it could exceed 11,000 points before the year is out. Somewhat surprisingly, British investors are unconvinced, however. They pulled almost £10bn from UK-focused funds last year, marking a decade of consecutive withdrawals, with the US still much in favour.

A very troubled global picture continues to confront us; However, the UK is on a roll. The UK FTSE 100 index rose by more than a fifth in 2025, beating both the US and Europe in local currency terms. It has gone on to hit new highs in January, and analysts think it could exceed 11,000 points before the year is out. Somewhat surprisingly, British investors are unconvinced, however. They pulled almost £10bn from UK-focused funds last year, marking a decade of consecutive withdrawals, with the US still much in favour.

Technology companies account for roughly 3% of the FTSE 100, compared with a third of the S&P 500. This is a key reason why the UK has significantly lagged behind North America over the past decade, from both a returns and valuation perspective. However, the FTSE 100’s ‘old fashioned’ status is starting to work in its favour. Higher interest rates have turbocharged banks after years of underperformance. Meanwhile, miners are reaping the rewards of higher gold, silver and copper prices. Another standout sector is defence, which has been boosted by higher military spending across Europe, although not a sector that is compatible with ESG investors.

The question is whether these trends have further to run. Miners form an important part of the FTSE 100, but they are notoriously cyclical. If metal prices drop in 2026, miners will quickly feel the effect.

The geopolitical outlook will also play an important role this year. We have already seen investors in defence stocks briefly lose their nerve during peace talks between Ukraine and Russia. If global tensions ease this year, this could knock the UK’s aerospace and defence industry, which represents about 8% of the FTSE 100.

Similarly, investors will be watching to see if lower interest rates will hit the banking sector, which massively outperformed in 2025. The expectation is for a further rate cut in March following four cuts in 2025. A Panmure Gordon analyst flagged that the FTSE 100’s recent outperformance is concentrated in a small number of stocks, which could increase risk. “If the rally in banks or defence stocks stalls, the FTSE 100 may quickly become an underperformer again,” he said. We are very familiar with concentration as it is particularly prevalent with the ‘Magnificent 7’ in the US market.

We have continuously had exposure to the UK in almost all portfolios but have preferred the All Companies sector rather than the more concentrated FTSE 100. Whilst the UK has performed well we have seen better opportunities in other global markets for many years. We will continue to watch but we share the concerns of Panmure Gordon’s analyst.

The AI Revolution

Towards the end of last year, much was reported regarding a potential AI bubble that was set to burst. Several well-known figures in the financial world including the governor of the Bank of England and the Chief Executive of JP Morgan both voiced such concerns. Jamie Dimon, Chairman and CEO of JPMorgan Chase, expressed a more nuanced view on artificial intelligence, stating that while the technology itself is not a bubble, the extreme market enthusiasm surrounding it has created “bubble-like” conditions in certain areas. As of late 2025 and early 2026, Dimon has characterized AI as a transformative, long-term trend rather than a passing fad, comparing its potential impact to the early days of the internet. While he was bullish on AI’s potential, Dimon cautioned that some AI-related assets and projects are likely in a bubble, with valuations that may not hold up. Despite short-term concerns about over-investment in some projects, Dimon has maintained that the overall AI investment cycle will “probably pay off” in the long run.

Many asset managers did not share these views albeit recognised values were high but, in their view, so was the substantial earning potential. Over the last few weeks, we have seen the focus of the “attack” change. The attack is now very focussed on companies that might be casualties of the AI revolution. “We are in the midst of a market regime change driven by an AI narrative that is hell bent on creating as many AI losers as AI winners” said a leading global fund manager at Rathbones (Source: Rathbone Global Opportunities fund – Monthly Update January 2026). “The dislocation in some stocks and sectors is the greatest I have seen in my 25-year career. Witness the cratering of the broader global software and information services sector. US software has undergone the largest non-recessionary 12-month drawdown relative to the broader market in over 30 years (-34% in Sterling terms)”.

“At the moment, narrative outweighs fundamentals. Some share prices are assuming 0% revenue growth and zero terminal value – essentially labelling these ‘typewriter’ (a new term for us) companies as AI eats everything. We see opportunities emerging from the meltdown, particularly in cybersecurity software companies that have been inexplicably caught up in this thematic unwind, but in a market with a ‘guilty until proven innocent’ vibe it will probably require a noticeable growth acceleration to convince investors of the upside potential”.

A recent post written by tech entrepreneur and investor Matt Shumer went viral on social media (Source: Bloomberg – ‘The AI Panic Ignores Something Important – The Evidence’). It was a rundown of all the ways artificial intelligence would, in short order, decimate professional jobs. Tools like Claude Code and Claude Cowork from Anthropic PBC, probably unfamiliar names to most of us right now but that may quickly change, would displace the work of lawyers and wealth managers, he wrote.

Shumer’s post has struck a nerve in the middle of a sell-off of finance and software companies whose products seem ripe for disruption from AI, as the Rathbone’s manager reported. However, take a breath. A slow and deliberate approach to the nuanced impact of AI is needed today, as well as some humility over the fact that none of us – not even the AI labs – have any idea what is around the corner. OpenAI’s leaders didn’t expect ChatGPT to spark a market boom and Anthropic was shocked at the impact of its latest products.

Two things can be true at the same time: AI’s impact can be both overhyped and real. But striking that balance means prioritizing evidence over testimony and tracking things like productivity statistics and hiring rates. We’ve seen this pattern before. When stories got ahead of reality in the early 2000s, we got the dot-com crash. The Internet turned out to be as transformative as people claimed, but it took longer than expected to play out.

Artificial intelligence is a genuinely useful technology, but its impact will be uneven, gradual and impossible to predict. That’s the boring truth; however unlikely it is to go viral. Despite the hype, underlying data such as national productivity statistics and labour market trends have not changed significantly, and experts are advising a slow and deliberate approach to understanding the impact of AI. We would concur and not jump to any conclusion which is most likely to be wrong and potentially expensive.

Douglas Kearney C.A. Investment Director

The above article is intended to be a topical commentary and should not be construed as financial advice. Past performance is not an indicator of future returns. Any news and/or views expressed within this document are intended as general information only and should not be viewed as a form of personal recommendation.