Trump’s First 100 Days

The only thing that is predictable is that the months ahead will be unpredictable. If the first two months of 2025 were dominated by the start of Donald Trump’s second term as President of the United States, the following two months, March and April, saw the threat of tariffs become a very stark reality. On the 2nd of April a swathe of tariffs was announced which sent the US and other markets tumbling. The most severe tariffs were inflicted on China at an eyewatering level of 145%. China had the audacity to retaliate which was not well received in the White House. The President recently indicated that trade talks are well underway with China but that appears to be news to China, who insist no such talks have commenced.

Stocks erased a combined $6.6 trillion in value on the Thursday and Friday following his Wednesday tariff announcement. Roughly $11.1 trillion has been wiped away from the U.S. stock market since 17th January 2025, the Friday before President Donald Trump took the oath of office and began his second term, according to data from Dow Jones Market Data. The Magnificent 7 were no longer magnificent and the wheels were coming off Elon Musk’s Tesla. Talk of iPhones retailing in the US at over $3,000 caused some alarm with consumers. That was never the plan, surely. Markets struggled with the huge uncertainty that he had created. It is impossible to find an independent economist who believes that the tariffs will be anything other than a significant dampener on global growth, with the USA likely to be hurt most by rising prices and significantly higher inflation.

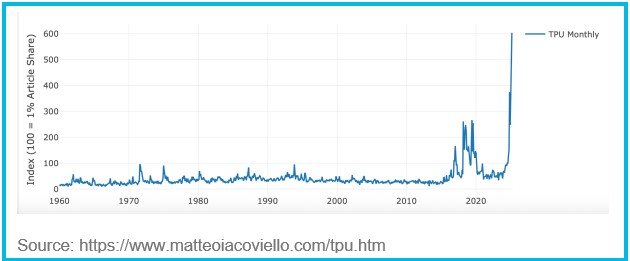

The TPU Index measures the level of uncertainty or unpredictability in a country’s trade policies at a given time.

The TPU Index measures the level of uncertainty or unpredictability in a country’s trade policies at a given time.

A high TPU index suggests businesses and investors are unsure about future tariffs, trade agreements, or regulations, impacting their decision-making. Unsurprisingly, it is at unprecedented levels just now and even in Trump’s first term it got nowhere as high as where it is today.

Why do US Government Bonds Matter?

Initially, following the so-called “Liberation Day” tariffs announcement on 2nd April 2025 when shares plunged, investors did appear to flock to US bonds as a safe haven. However, when the first of these tariffs kicked in on 5th April and Trump doubled down on his policies that weekend, investors began dumping government bonds, sending the interest rate the US government would have to pay to borrow money up sharply. The yield for US government borrowing over 10 years shot up from 3.9% to 4.5%, while the 30-year yield spiked at almost 5%. Movements of 0.2% in either direction are considered a big deal.

Despite indicating the man is not for turning, it was not long before the President announced there would be a delay in implementing the tariff policy, but he assured the world he was not backtracking. Really? Wall Street breathed a sigh of relief that Trump was backing down (no matter the reason) on other extreme trade measures. Stocks rallied sharply on the news – even though the 10% universal tariff on all imports coming into the US remained in effect. (Another market wobble was triggered later in the month when President Trump threatened to replace the Chairman of the Federal Reserve for not cutting interest rates. He insisted he had been misunderstood, and that Jerome Powell was not under threat – time will tell).

Investors around the world have for a long, long time considered Treasuries “so rock-solid safe they’re risk-free,” said Bloomberg. Trump’s “all-out assault on global trade” has put that status in question. Investors are dumping 10- and 30-year Treasuries alongside “stocks, crypto and other risky assets.” That’s because Treasuries depend on the US’s reputation for fiscal and monetary “competence,” said James Grant, the founder of Grant’s Interest Rate Observer. The volatility of the bond market suggests the “world is reconsidering.”

America’s “global safe-haven status is in question,” said J.P. Morgan Asset Management‘s Priya Misra to The New York Times. That questioning raised alarms in the White House. Trump pointed to bond market skittishness as the reason he paused most of his previously announced tariffs. That did not stop the damage. America is now “being treated by global financial markets like a problematic emerging market,” said former U.S. Treasury Secretary Lawrence H. Summers. A reputation under serious threat in less than a hundred days.

So, the uncertainty over the impact of tariffs on the US economy led to investors no longer seeing government bonds as such a safe bet, so demanded bigger returns to buy them. According to US media reports, it was Treasury Secretary Scott Bessent, inundated with calls from business leaders, who played a key part in swaying Trump. “Although President Donald Trump was able to resist the stock market sell-off, once the bond market began to weaken too, it was only a matter of time before he folded,” says Paul Ashworth, chief North America economist at Capital Economics.

It proved a pressure point for Trump – and now the world knows it. It also demonstrated a brake existed.

Some analysts suggested that America’s central bank, the US Federal Reserve, might have been forced to step in if the sell-off had worsened. While bond yields have settled, some might argue the damage has already been done as they remain higher than before the blanket tariffs kicked in. “Arguably the most worrying aspect of the [recent] turmoil… is an emerging risk premium in US Treasury bonds and the dollar, akin to what the UK experienced in 2022,” according to Jonas Goltermann, deputy chief markets economist at Capital Economics.

Some analysts suggested that America’s central bank, the US Federal Reserve, might have been forced to step in if the sell-off had worsened. While bond yields have settled, some might argue the damage has already been done as they remain higher than before the blanket tariffs kicked in. “Arguably the most worrying aspect of the [recent] turmoil… is an emerging risk premium in US Treasury bonds and the dollar, akin to what the UK experienced in 2022,” according to Jonas Goltermann, deputy chief markets economist at Capital Economics.

In times like these it is prudent to stay calm and remain invested. There is plenty of evidence that staying invested has been the sensible policy. It would be optimistic to believe the uncertainty and volatility will be lifted any time soon, but volatility is normal albeit uncomfortable at times. In the 129-year history of the Dow Jones Industrial Average, the index has closed higher or lower by at least 1,000 points just 31 times. Four of those times happened in the first week of April. It is calming down a little now but it is far from over.

Douglas Kearney C.A. Investment Director

The above article is intended to be a topical commentary and should not be construed as financial advice. Past performance is not an indicator of future returns. Any news and/or views expressed within this document are intended as general information only and should not be viewed as a form of personal recommendation.